The Hidden Rate-Cut Ripple Effect: What Banks Won’t Tell You About Refinancing Timing in a 5% World

Why the Standard Refinance Playbook is Broken in Austin, TX

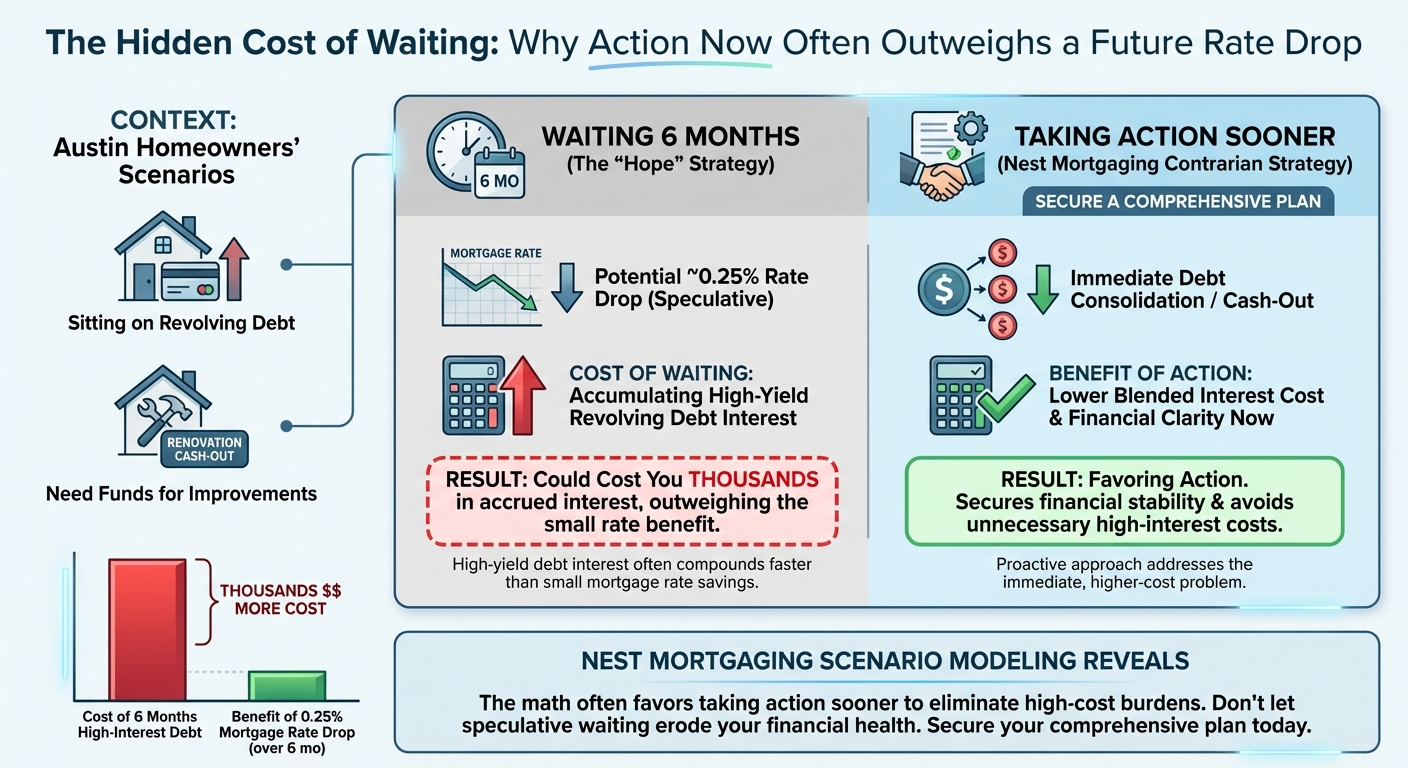

If you are waiting for mortgage rates to drop back to historic lows before refinancing your Austin area home, you might be falling into a costly trap. Welcome to the 5% world. Most big banks and traditional lenders are pushing a standard narrative to wait for the Federal Reserve to make a move, then rush to refinance. However, at Nest Mortgaging, we are seeing a different reality unfold.

The hidden rate-cut ripple effect means that the moment rates officially drop, a massive wave of pent-up demand floods the market. This surge can inflate home prices and increase competition, effectively canceling out your interest rate savings. Erica Bille and our team of Austin mortgage brokers use contrarian scenario modeling to help you time your move before the masses catch on.

- Beat the Rush: Act before the broader market reacts to rate adjustments.

- Leverage Equity: Use your current home equity to consolidate debt now.

- Custom Strategy: Get a tailored plan rather than a one-size-fits-all bank pitch.

Contrarian Scenario Modeling: The 5% Rate Environment

Let us look at the numbers no one else is publishing. When you factor in the cost of waiting, the math often favors taking action sooner. Many homeowners in Austin, TX are sitting on high-interest credit card debt or need to pull cash out for renovations. Waiting six months for a potential quarter-point drop in mortgage rates could cost you thousands in high-yield revolving debt interest.

Our scenario modeling at Nest Mortgaging reveals a fascinating contrarian timing strategy. By securing a competitive rate now with one of our 60 plus lenders, you can instantly improve your monthly cash flow. We pride ourselves on precision and detail, ensuring your tailored loan solution aligns perfectly with your financial goals.

| Scenario | Interest Rate | Monthly Payment | Total Interest Paid (5 Yrs) | Opportunity Cost |

|---|---|---|---|---|

| Wait 12 Months for Rate Drop | 4.85% | $2,650 | $85,000 | $12,000 in lost savings |

| Refinance Now (Debt Consolidation) | 5.25% | $2,710 | $92,000 | $0 (Immediate Cash Flow) |

| Wait 24 Months (Market Surge) | 4.75% | $2,610 | $83,500 | $24,000 in lost savings |

How Nest Mortgaging Can Help You Time the Market

Timing is everything, and simplicity meets speed when you work with a dedicated local expert. At Nest Mortgaging, we offer a 14-day average closing time and boast a 100 percent customer satisfaction rate. Erica Bille and our team prioritize real human connection, providing honest and unbiased advice to guide you through the complexities of the mortgage process.

We have helped countless Texas homebuyers and homeowners optimize their finances. Whether you want to lower your monthly payment or take cash out, our team specializes in market trends to determine the precise time to act. Do not let the big banks dictate your financial future with outdated advice.

Q1: What is the rate-cut ripple effect?

The rate-cut ripple effect occurs when an anticipated drop in interest rates triggers a massive surge in buyer demand and refinancing applications, which can increase closing times and offset interest savings due to rising costs.

Q2: Should I wait for mortgage rates to drop below 5 percent in Austin?

Not necessarily. Waiting for rates to drop can cost you more in the long run if you are currently paying high interest on credit cards or personal loans. Refinancing now to consolidate debt can improve your immediate cash flow.

Q3: How long does the refinancing process take with Nest Mortgaging?

We pride ourselves on speed and efficiency. Nest Mortgaging offers a streamlined loan experience with an impressive 14-day average closing time.

Q4: Why choose a mortgage broker over a traditional bank?

Traditional banks offer limited, one-size-fits-all products. As an independent Austin mortgage broker, Erica Bille and Nest Mortgaging have access to over 60 different lenders, allowing us to find highly competitive and tailored loan solutions.

Q5: Can I refinance to take cash out for home improvements?

Absolutely. Cash-out refinancing is a powerful tool in a 5 percent rate environment, allowing you to leverage your home equity for renovations, debt consolidation, or other major expenses.

Ready to explore your personalized refinancing options? Schedule a consultation with Erica Bille and Nest Mortgaging today to get a quick custom quote and discover how our contrarian strategies can save you money.